SVR¶

SVR (Support Vector Regression) solves the following optimization problem:

\[\min_{\mathbf{\beta} \in \mathbb{R}^d} \sum_{i=1}^{n} (|y_i - \mathbf{x}_i^\intercal \mathbf{\beta}| - \epsilon)_+ + \frac{\lambda}{2} \|\mathbf{\beta}\|^2\]

where \(\mathbf{x}_i \in \mathbb{R}^d\) is a feature vector, and \(y_i \in \mathbb{R}\) is a continuous response variable.

[2]:

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

import seaborn as sns

import warnings

from sklearn.datasets import make_regression

from sklearn.preprocessing import StandardScaler

[3]:

# Simulate data

np.random.seed(42)

scaler_svr = StandardScaler()

n, d = 10000, 5

X, y = make_regression(n_samples=n, n_features=d, noise=1.0)

X = scaler_svr.fit_transform(X)

X = np.hstack((X, np.ones((n, 1)))) # add intercept

y = y / y.std()

[4]:

## solve SVR via `plqERM_Ridge`

from rehline import plqERM_Ridge

clf = plqERM_Ridge(loss={'name': 'svr', 'epsilon': 0.1}, C=1.0)

clf.fit(X=X, y=y)

[4]:

plqERM_Ridge(loss={'epsilon': 0.1, 'name': 'svr'})In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

plqERM_Ridge(loss={'epsilon': 0.1, 'name': 'svr'})[5]:

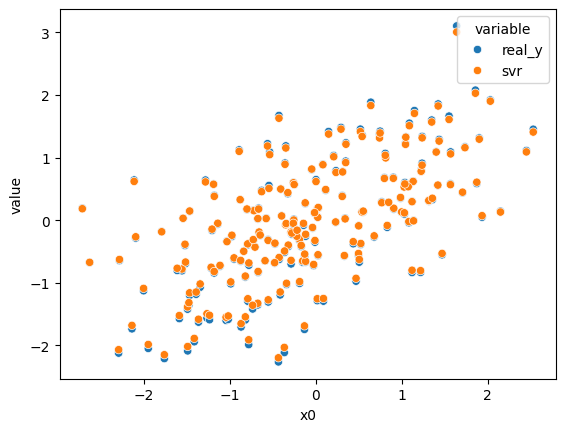

## plot SVR results

warnings.filterwarnings("ignore", "is_categorical_dtype")

n_sample = 200

X_sample, y_sample = X[:n_sample], y[:n_sample]

svr_sample = clf.decision_function(X_sample)

df = pd.DataFrame({'x0': X_sample[:,0], 'real_y': y_sample, 'svr': svr_sample})

df = df.melt(id_vars='x0')

sns.scatterplot(data=df, x='x0', y='value', hue='variable')

plt.show()