Getting Started¶

This page provides a starter example to introduce users to the rehline package and showcase its primary features, facilitating exploration and familiarization.

To proceed, ensure that you have already installed rehline:

pip install rehline

rehline is a versatile solver for machine learning problems, particularly effective for Empirical Risk Minimization (ERM) with non-smooth objectives. We will use ERM as our starting example to demonstrate that:

Note

With rehline, you can easily transform different loss functions and add constraints to your ERM with no tears!

Let’s begin by generating a toy dataset and splitting it into training and test sets using scikit-learn’s make_regression.

# Import necessary libraries

import numpy as np

from sklearn.datasets import make_regression

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

np.random.seed(1024)

# Generate toy data

n, d = 1000, 5

scaler = StandardScaler()

X, y = make_regression(n_samples=n, n_features=d, noise=1.0)

# Normalize X and add intercept

X = scaler.fit_transform(X)

X = np.hstack((X, np.ones((n, 1))))

# Split data into training and test sets

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=50)

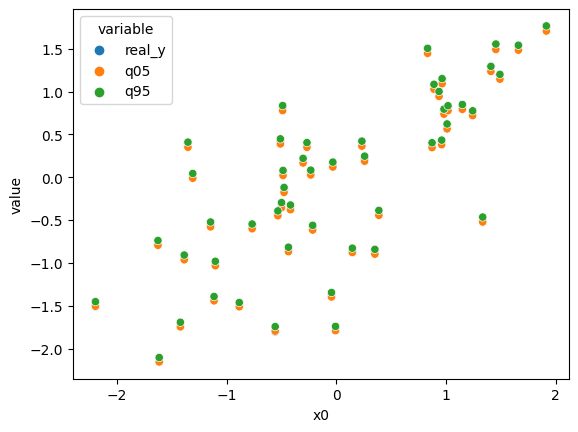

Quantile Regression¶

Next, let’s use rehline to fit a quantile regression (QR) at quantile level 0.95 (\(\kappa=0.95\)).

The ridge-regularized QR solves the following optimization problem:

where \(\rho_\kappa(u) = u \cdot (\kappa - \mathbf{1}(u < 0))\) is the check loss, \(x_i \in \mathbb{R}^d\) is a feature vector, and \(y_i \in \mathbb{R}\) is the response variable.

Since the check loss is a piecewise linear quadratic function (PLQ), it can be solved using rehline.plqERM_Ridge:

from rehline import plqERM_Ridge

# Define a QR estimator

clf = plqERM_Ridge(loss={'name': 'QR', 'qt': 0.95}, C=1.0)

clf.fit(X=X_train, y=y_train)

# Make predictions

q_predict = clf.decision_function(X_test)

# Plot results

import matplotlib.pyplot as plt

plt.scatter(x=X_test[:, 0], y=y_test, label='y_true')

plt.scatter(x=X_test[:, 0], y=q_predict, alpha=0.5, label='q_95')

plt.legend(loc="upper left")

plt.show()

Huber Regression¶

If you prefer Huber regression, it is also a PLQ function.

The ridge-regularized Huber minimization solves the following optimization problem:

where \(H_\kappa(\cdot)\) is the Huber loss defined as follows:

from rehline import plqERM_Ridge

# Define a Huber estimator

clf = plqERM_Ridge(loss={'name': 'huber', 'tau': 0.5}, C=1.0)

clf.fit(X=X_train, y=y_train)

# Make predictions

y_huber = clf.decision_function(X_test)

# Plot results

import matplotlib.pyplot as plt

plt.scatter(x=X_test[:, 0], y=y_test, label='y_true')

plt.scatter(x=X_test[:, 0], y=y_huber, alpha=0.5, label='y_huber')

plt.legend(loc="upper left")

plt.show()

Fairness Constraints¶

You have now learned that the fitted Huber regression requires a fairness constraint for the first feature \(\mathbf{X}_{1}\). Specifically, the correlation between the predicted \(\hat{Y}\) and \(\mathbf{X}_{1}\) must be less than tol=0.1, that is,

With rehline, you can easily add a fairness constraint to your ERM.

from rehline import plqERM_Ridge

from scipy.stats import pearsonr

# Define a Huber estimator with fairness constraint

clf = plqERM_Ridge(loss={'name': 'huber', 'tau': 0.5},

constraint=[{'name': 'fair', 'sen_idx': [0], 'tol_sen': 0.1}],

C=1.0,

max_iter=10000)

clf.fit(X=X_train, y=y_train)

# Make predictions

y_huber_fair = clf.decision_function(X_test)

# Plot results

import matplotlib.pyplot as plt

plt.scatter(x=X_test[:, 0], y=y_test, label='y_true')

plt.scatter(x=X_test[:, 0], y=y_huber, alpha=0.5, label='y_huber')

plt.scatter(x=X_test[:, 0], y=y_huber_fair, alpha=0.5, label='y_huber_fair')

plt.legend(loc="upper left")

plt.show()

Related Examples