ReHLine: Empirical Risk Minimization¶

The objective function is given by the following PLQ formulation, where \(\phi\) is a convex piecewise linear function and \(\lambda\) is a positive regularization parameter.

\[\min_{\pmb{\beta} \in \mathbb{R}^d} \sum_{i=1}^n \text{PLQ}(y_i, \mathbf{x}_i^T \pmb{\beta}) + \frac{1}{2} \| \pmb{\beta} \|_2^2, \ \text{ s.t. } \

\mathbf{A} \pmb{\beta} + \mathbf{b} \geq \mathbf{0},\]

where \(\text{PLQ}(\cdot, \cdot)\) is a convex piecewise linear quadratic function, see Loss for built-in loss functions, and \(\mathbf{A}\) is a \(K \times d\) matrix, and \(\mathbf{b}\) is a \(K\)-dimensional vector for linear constraints, see Constraints for more details.

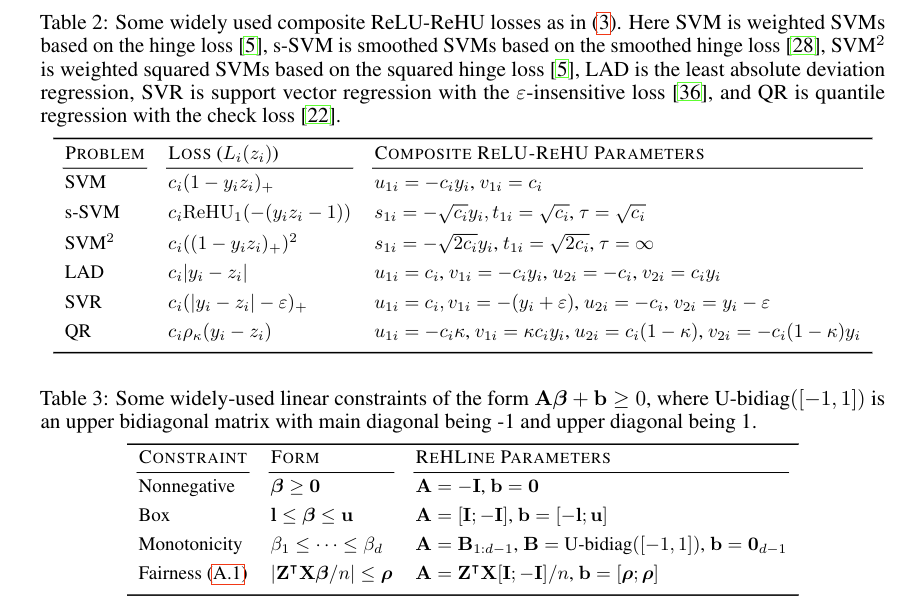

For example, it supports the following loss functions and constraints.

Example¶

Empirical Risk Minimization