Ridge Composite Quantile Regression¶

The regularized composite quantile regression solves the following optimization problem:

\[min_{\beta \in \mathbb{R}^{d}, \alpha \in \mathbb{R}^{K}} \ C \sum_{k=1}^K \sum_{i=1}^n \rho_\kappa ( y_i - x^\intercal_i \beta - \alpha_k) + \frac{1}{2} (\| \beta \|^2 + \| \alpha \|^2),\]

where \(\alpha_k\) is the intercept associated with k-th quantile, \(\rho_\kappa(u) = u\cdot(\kappa - \mathbf{1}(u < 0))\) is the check loss, \(x_i \in \mathbb{R}^d\) is a feature vector, \(y_i \in \mathbb{R}\) is the response variable.

[10]:

## simulate data

from sklearn.datasets import make_regression

from sklearn.preprocessing import StandardScaler

scaler = StandardScaler()

n, d = 1000, 1

X, y, coef = make_regression(n_samples=n, n_features=d, noise=50.0, coef=True)

X = scaler.fit_transform(X)

y = y / y.std()

[11]:

## fit model

from rehline import CQR_Ridge

cqr = CQR_Ridge(quantiles=[0.05, 0.5, 0.95])

cqr.fit(X, y)

y_pred = cqr.predict(X) # 3 columns, each represents the prediction for a quantile

[12]:

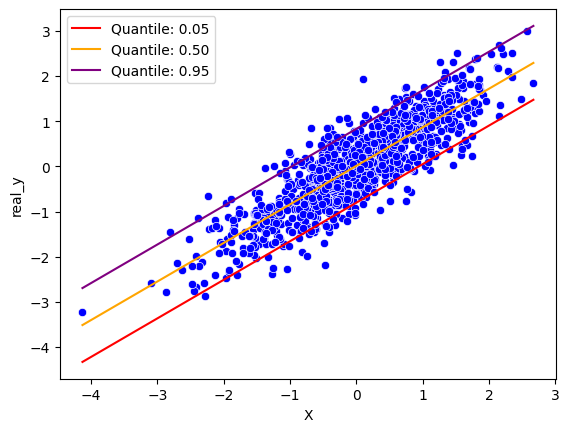

## plot QR results

import matplotlib.pyplot as plt

import pandas as pd

import seaborn as sns

df = pd.DataFrame({"X": X.squeeze(), "real_y": y, "q05": y_pred[:, 0], "q50": y_pred[:, 1], "q95": y_pred[:, 2]})

## scatter plot of the data

sns.scatterplot(df, x="X", y="real_y", color="blue")

## plot the quantile regression lines

sns.lineplot(df, x="X", y="q05", color="red", label="Quantile: 0.05")

sns.lineplot(df, x="X", y="q50", color="orange", label="Quantile: 0.50")

sns.lineplot(df, x="X", y="q95", color="purple", label="Quantile: 0.95")

plt.show()