Custom QR¶

The Custom QR solves the following optimization problem:

\[\min_{\mathbf{\beta} \in \mathbb{R}^d}

C\sum_{i=1}^n \rho_{\kappa}(y_i-\mathbf{x}_i^\top\mathbf{\beta})

+\frac{1}{2}\|\mathbf{\beta}\|_2^2,\]

\[\text{subject to} \quad A\mathbf{\beta}+b \ge 0,\]

where:

\(\mathbf{x}_i \in \mathbb{R}^d\) is a feature vector

\(y_i \in \mathbb{R}\) is a continuous response variable

\(\rho_{\kappa}(u)=u\big(\kappa-\mathbf{1}(u<0)\big)\) is the quantile (check) loss

\(A \in \mathbb{R}^{K \times d}\) and \(b \in \mathbb{R}^{K}\) define custom linear constraints

The custom constraints allow arbitrary prior knowledge (e.g. sign, ordering, budget, or linear relation constraints) to be incorporated into quantile regression.

Note. Since the check loss is a plq function and the constraints are linear (\(A\beta+b\ge0\)), we can optimize it using

rehline.plq_Ridge_Regressor.

[ ]:

## install rehline

%pip install rehline -q

[2]:

## simulate data

from sklearn.datasets import make_regression

from sklearn.preprocessing import StandardScaler

import numpy as np

scaler = StandardScaler()

n, d = 10000, 5

X, y = make_regression(n_samples=n, n_features=d, noise=1.0, random_state=42)

X = scaler.fit_transform(X)

y = y / y.std()

[3]:

# Example: beta_0 + beta_1 >= 3

A = np.zeros((1, d))

A[0, 0] = 1

A[0, 1] = 1

b = np.array([-3.0])

QR as baseline¶

[4]:

## we first run a QR

from rehline import plq_Ridge_Regressor

clf = plq_Ridge_Regressor(

loss={'name': 'QR', 'qt': 0.5},

C=1.0,

max_iter=10000,

fit_intercept=False

)

clf.fit(X=X, y=y)

[4]:

plq_Ridge_Regressor(fit_intercept=False, max_iter=10000)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

plq_Ridge_Regressor(fit_intercept=False, max_iter=10000)

Custom Constraint¶

[5]:

## solve custom via `plq_Ridge_Regressor` by adding `constraint`

from rehline import plq_Ridge_Regressor

cclf = plq_Ridge_Regressor(

loss={'name': 'QR', 'qt': 0.5},

constraint=[{'name': 'custom', 'A': A, 'b': b}],

C=1.0,

max_iter=10000,

fit_intercept=False

)

cclf.fit(X=X, y=y)

[5]:

plq_Ridge_Regressor(constraint=[{'A': array([[1., 1., 0., 0., 0.]]),

'b': array([-3.]), 'name': 'custom'}],

fit_intercept=False, max_iter=10000)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

plq_Ridge_Regressor(constraint=[{'A': array([[1., 1., 0., 0., 0.]]),

'b': array([-3.]), 'name': 'custom'}],

fit_intercept=False, max_iter=10000)[6]:

import pandas as pd

## score

score = clf.predict(X)

cscore = cclf.predict(X)

qr_perf = np.mean((y - score)**2)

cqr_perf = np.mean((y - cscore)**2)

# Create a pandas DataFrame to store the results

results = pd.DataFrame({

'Model': ['QR', 'Custom QR'],

'Train MSE': [qr_perf, cqr_perf]

})

# Print the results as a table

print(results.to_string(index=False))

#Print the results of custom constraint

lhs = cclf.coef_[0] + cclf.coef_[1]

print(f"\ncoef_0 + coef_1 = {lhs:.8f} >= 3: {lhs >= 3}")

Model Train MSE

QR 0.000097

Custom QR 1.352705

coef_0 + coef_1 = 3.00000008 >= 3: True

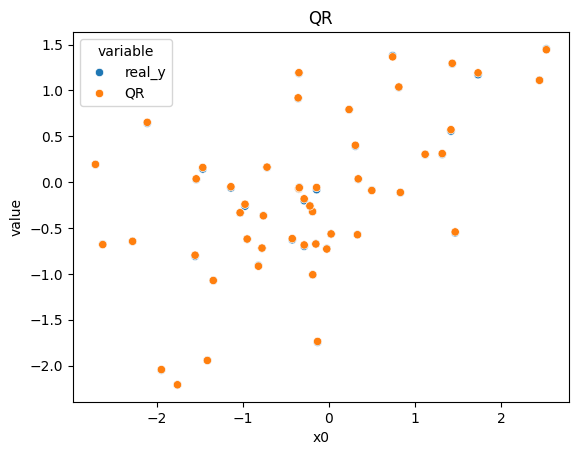

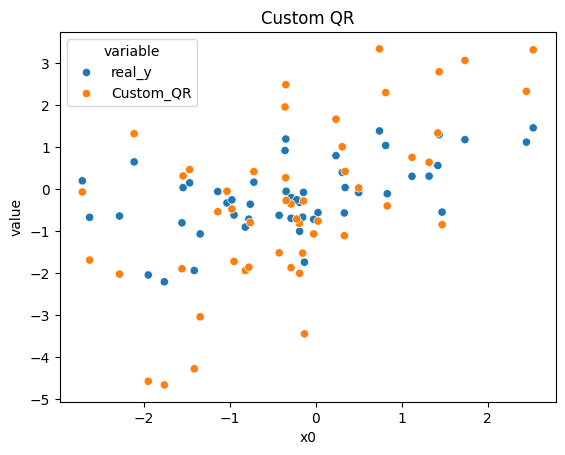

[7]:

import seaborn as sns

import pandas as pd

import warnings

import matplotlib.pyplot as plt

warnings.filterwarnings("ignore", "is_categorical_dtype")

warnings.filterwarnings("ignore", "use_inf_as_na")

n_sample = 50

X_sample, y_sample = X[:n_sample], y[:n_sample]

qr_sample = clf.predict(X_sample)

cqr_sample = cclf.predict(X_sample)

df = pd.DataFrame({

'x0': X_sample[:, 0],

'real_y': y_sample,

'QR': qr_sample,

'Custom_QR': cqr_sample

})

df1 = df[['x0', 'real_y', 'QR']].melt(id_vars='x0')

sns.scatterplot(data=df1, x='x0', y='value', hue='variable').set_title("QR")

plt.show()

df2 = df[['x0', 'real_y', 'Custom_QR']].melt(id_vars='x0')

sns.scatterplot(data=df2, x='x0', y='value', hue='variable').set_title("Custom QR")

plt.show()